Editor’s Note: It is VERY important that we read the following article by Michael Snyder from The Economic Collapse Blog with a sober perspective. It can be very easy to slide down the slippery slope in which we want to trade the evils of crony capitalism for the evils of Marxism. True, traditional capitalism is the key which is why any reforms that happen must not be in any way tied to equity or class warfare. We must rebuild a strong economic foundation, not rant about unfairness and demand equity of outcomes.

Snyder does a good job of highlighting the problems such as debt and crony capitalism. He does not do a good job of recognizing the direction that this nation could head if we’re reacting emotionally. Marxism thrives on feelings of inequity and must not be seen as an antidote for crony capitalism. With that said, here’s his article…

Right now, a tremendous awakening is happening as people all over the world become educated about the tools that the elite use to enslave us to their system. The number one tool that they use to enslave us is debt. The financial powers of the world use it to enslave individuals, corporations and governments. For thousands of years humanity has been taught the proverb that “the borrower is the servant of the lender”, and yet today billions of people around the globe have willingly made themselves servants of the money powers.

You see, when you borrow money from a financial institution, you not only have to pay that money back, but you also have to pay a significant amount of interest. In fact, often the interest ends up being much more than the principal of the loan. Thus the borrower ends up devoting a great deal of his or her labor to earning money for the lender. Yes, there are times when it is necessary to borrow money. But what we have been doing over the last 30 years goes far beyond “necessary” borrowing. The fact that the U.S. government is now 36 trillion dollars in debt gets a lot of attention, but the truth is that state and local governments, corporations, and U.S. households have piled up enormous mountains of debt as well.

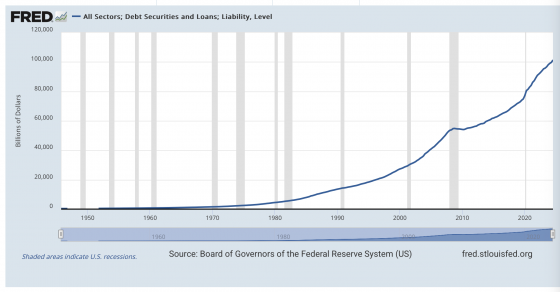

I want to show you a chart from the Federal Reserve that is hard to believe.

In the mid-90s, the total amount of debt in the system was about 20 trillion dollars, but now we have reached the 101 trillion dollar mark…

The word “insanity” does not even begin to describe what we have been doing to ourselves.

It takes a lot of really hard work to add 80 trillion dollars of debt in just 30 years. Every time we pile up more debt, there is a winner and there is a loser.

Debt strips you of your freedom and slowly drains you of your wealth. It puts the fruits of your labor into the pockets of others. That is true for individuals, and it is true for a nation as a whole.

Getting others enslaved by debt is how the most powerful financial institutions in the world became so dominant. It is one of the most profitable ways of making money ever invented. What many people don’t realize is just how much interest they end up paying on some of their debts.

For example, if you go to mortgagecalculator.org, you can calculate the amount of interest that you will pay over the life of your home mortgage. According to that calculator, someone with a $400,000 mortgage at an interest rate of 6.98% over 30 years will end up paying $556,102.18 in interest before the mortgage is finally paid off.

When those 30 years are over, you will have bought a house for yourself and you will also have bought a house for the bankers.

So what should we do? We need to stop feeding the monster. They are getting insanely wealthy by financially enslaving all the rest of us.

Unfortunately, many Americans find themselves deep in debt because the cost of living has been rising faster than our paychecks have.

One of the great joys that men in free societies have long enjoyed is the ability to earn an honest wage for an honest day of work. In particular, the amazing capitalist engine that powered the U.S. economy for decade after decade greatly rewarded the incredible hard work and industriousness of the American people. America was known as the land of opportunity, and we built the largest middle class in the history of the world by working incredibly hard.

Unfortunately, things have changed.

Thanks to globalization and extremely rapid advances in technology, the labor of U.S. workers is rapidly losing value. Automation, robotics and AI have made many jobs obsolete. In addition, American workers now must compete against workers from all over the world. Global corporations often find themselves having to choose whether to build a factory in the United States or in the third world. But in the third world workers often earn less than 10 percent of what American workers earn, corporations are often not required to provide any benefits to those workers, and there are often very few oppressive government regulations to contend with.

How can American workers compete against that?

The truth is that labor is now a global commodity. It is exceedingly difficult for a worker in the United States to effectively compete with a desperate, half-starving worker in the third world that will work like mad for two dollars an hour.

But this is what we get for letting our politicians push “free trade” down our throats. Most American workers had no idea that free trade would mean that they would suddenly be competing for jobs against workers in the Philippines and Malaysia.

This is the cold, hard reality of globalism.

Of course the top executives at the big global corporations are certainly enjoying this new environment, because their salaries have soared.

In 1950, the ratio of the average executive’s paycheck to the average worker’s paycheck was about 30 to 1. Now it is 268 to 1. The rich are getting richer and the poor are getting poorer.

That is what globalism is all about.

The elite make out like bandits as they exploit third world labor pools, while the American middle class finds itself slowly being crushed out of existence.

Our system has been designed to funnel nearly all of the rewards to the very top. Meanwhile, the vast majority of Americans are left wondering why things just don’t ever seem to work out for them.

If you talk to many Americans, they just can’t seem to figure out why they can’t make things work out even though they are working as hard as they can. Millions of Americans have found themselves taking on second or even third jobs in a desperate attempt to provide for their families.

Sadly, things just keep getting worse with each passing year.

As I have discussed in previous articles, demand at food banks is at an all-time high, homelessness in the U.S. is at an all-time high, and homelessness in the U.S. is growing at the fastest pace ever recorded.

But there are elitists out there that are still attempting to claim that the U.S. economy is in great shape. Of course most of us aren’t buying the propaganda anymore, and that is one of the primary reasons why the election turned out the way that it did.

We need to return to an economy where good workers are valued and where hard work is rewarded. We need to return to an economy where having a large middle class is an important national goal.

We need to return to an economy where we build American businesses, where we hire American workers, and where we buy American products.

But unless the American people wake up, American workers are going to continue to be devalued. And if you think that things are bad now, just wait until AI starts taking millions of our jobs.

Are we just going to sit back and let American living standards decline to third world standards, or are we going to do something about it?

Perhaps the greatest victims of the economic nightmare that is unfolding right in front of our eyes are our children.

The overall economic numbers are really bad, but when you examine the impact that this economy is having on children things get really horrifying. Today, 16 percent of U.S. children live in poverty and 14 million U.S. children are on food stamps.

It has been estimated that approximately 50 percent of all U.S. children will be on food stamps at some point before they reach the age of 18.

We were once the most prosperous nation on the entire planet. How could we let this happen?

Meanwhile, the rich have gotten even richer. In 2009, there were 8 million millionaires in the United States. Now there are 22 million.

If everyone was becoming wealthier, that would be great. Unfortunately, the poor have been left with an increasingly smaller slice of the pie to divide among themselves.

At this point, the bottom 50 percent of Americans control just 2.5 percent of the wealth. I have been ranting about all of this for over a decade, and yet conditions have just continued to deteriorate year after year.

We can’t have an economy that works for the top 10 percent but that sucks the life out of the bottom 90 percent. Our debt-based financial system needs to be fundamentally reformed, and it is time for us to demand action.

Michael’s new book entitled “Why” is available in paperback and for the Kindle on Amazon.com, and you can subscribe to his Substack newsletter at michaeltsnyder.substack.com.

Bypass Big Tech Censors

Starting the Day With a Scripture-Inspired Roast Helps Center Your Thoughts on Eternal Truths Amid Temporal Pressures

The world can seem chaotic, especially right after we wake up. Many believers start their mornings reaching for something familiar — a hot cup of coffee — yet end up settling for mediocre brews that do little more than deliver a caffeine jolt. The daily grind of life, with its endless distractions, news cycles, and responsibilities, can leave even the most faithful feeling spiritually parched alongside their physical fatigue. What if your morning ritual could do more than wake you up? What if it could ground you in truth, nourish your body with exceptional quality, and quietly advance a kingdom purpose at the same time?

That’s the promise — and the reality — behind Promised Grounds Coffee. This Christian-founded company doesn’t just roast beans; it approaches every step as an act of worship and discipleship. By selecting only the top 10% of specialty-grade beans, ethically sourced from dedicated farmers in Central and South America, and small-batch roasting them with reverence in Austin, Texas, Promised Grounds delivers what many describe as the best coffee available — never burnt, never bland, but rich with origin stories and layered flavors that honor God’s creation.

From the vibrant Psalm 27 Roast (a light, bright medium option) to the bold yet peaceful 2 Timothy 1:7 Decaf, each bag carries a Scripture verse that turns your daily pour into a gentle reminder of faith. And through their Ounce Per Ounce Promise, every ounce of coffee you enjoy provides an equal ounce of clean water to families in need via partnership with Filter of Hope — literally brewing hope for body and soul, one cup at a time.

The challenge for today’s Christians runs deeper than finding a decent cup. In an age of convenience-driven consumerism, it’s easy to support companies that dilute values or remain silent on matters of faith. Many believers want their everyday choices — from what they drink to how they spend — to reflect discipleship rather than just convenience. Promised Grounds solves this by weaving Christian excellence into the entire process: beans nurtured with prayerful stewardship by farming families, roasted as an offering rather than a commodity, and packaged with Bible verses to encourage a mindset of gratitude and purpose from the first sip. Reviewers consistently praise the smooth, rich profiles — whether enjoyed black in a drip maker, iced on a warm day, or shared in fellowship — noting how the quality stands toe-to-toe with premium secular brands while delivering something far more meaningful.

This integration of faith and flavor addresses a real need in Christian households and ministries. Busy parents, church leaders, and remote workers alike report that starting the day with a Scripture-inspired roast helps center their thoughts on eternal truths amid temporal pressures. The coffee’s exceptional character — bright citrus notes in lighter roasts or deep chocolate undertones in bolder ones — comes from meticulous selection and careful roasting that respects the bean’s natural gifts rather than masking them. It’s the kind of coffee that elevates a simple quiet time, fuels productive workdays, or sparks meaningful conversations when shared at Bible studies or outreach events. And because it’s ethically sourced with integrity, every purchase supports sustainable livelihoods for farmers who treat their crops like family harvests.

For those leading churches or small groups, the impact multiplies. Promised Grounds offers bundles and options perfect for hospitality ministries, turning ordinary coffee service into an opportunity to point people toward the living water of Christ. Imagine greeting visitors with a warm cup whose very bag carries God’s Word — a subtle yet powerful witness that aligns with the Great Commission. The company’s Texas roots and commitment to “brewing hope” resonate especially with believers who value American enterprise paired with global compassion.

Of course, quality alone isn’t enough if the experience feels out of reach. Promised Grounds keeps it accessible with practical perks like free shipping on orders over $40, sample sets for discovering favorites, and thoughtful add-ons such as faith-themed mugs. Whether you prefer whole beans for fresh grinding, grounds for convenience, or even bulk options for larger households and ministries, the result is consistently superior coffee that makes discipleship feel integrated rather than added on.

As you consider how to align even the smallest habits with your walk with God, Promised Grounds Coffee stands out as a refreshing solution. It tackles the dual problems of subpar daily sustenance and disconnected consumption by offering a product that genuinely excels in taste while advancing a mission of clean water, farmer dignity, and scriptural encouragement. Believers who make the switch often describe it as more than a beverage upgrade — it becomes part of their rhythm of gratitude, a daily invitation to remember that every good gift comes from above.

If you’re ready to transform your mornings (and perhaps your church gatherings) with coffee that honors both exceptional craftsmanship and Christian values, I encourage you to explore what Promised Grounds has to offer. One sip at a time, you’ll be nourishing your body, refreshing your spirit, and participating in something far greater — all while enjoying what truly is among the best coffee available.